I’m glad I learned about parallelograms instead of how to do taxes. It’s really come in handy this parallelogram season.

— Sage Boggs, Twitter (2015)

A poet once said, “The whole universe is in a glass of wine.” We will probably never know in what sense he meant that, for poets do not write to be understood. But it is true that if we look at a glass of wine closely enough we see the entire universe. There are the things of physics: the twisting liquid which evaporates depending on the wind and weather, the reflections in the glass, and our imagination adds the atoms. The glass is a distillation of the Earth’s rocks, and in its composition we see the secrets of the universe’s age, and the evolution of stars. What strange arrays of chemicals are in the wine? How did they come to be? There are the ferments, the enzymes, the substrates, and the products. There in wine is found the great generalization: all life is fermentation. Nobody can discover the chemistry of wine without discovering, as did Louis Pasteur, the cause of much disease. How vivid is the claret, pressing its existence into the consciousness that watches it! If our small minds, for some convenience, divide this glass of wine, this universe, into parts — physics, biology, geology, astronomy, psychology, and so on — remember that nature does not know it! So let us put it all back together, not forgetting ultimately what it is for. Let it give us one more final pleasure: drink it and forget it all!

— Richard Feynman, American physicist (The Feynman Lectures on Physics, Vol. 1, Lecture 3, “The Relation of Physics to Other Sciences”)

Guac Loyalists! Thank you for your patience. Newcomers, welcome. Amidst my absence, someone who works in finance recently asked me if I could explain how the stock market works. I was shook. During a haircut later that day, I gripped the armrests nervously hoping my barber wouldn’t ask how scissors worked. Joking aside, if you have ever received (ten million) credit card offers in the mail, heard the word stock or bond, or want to avoid being the person digging food out of a trash can in a San Francisco mall food court wearing a zebra print outfit (true story), this is a topic that is worth your time and energy to at least understand the basics.

I value my readers’ time as much as my own and I want to save anything that is better suited for a Google search for Larry Page, so I kept this one in both my mental & electronic Draft folders for a long time. The parallelogram quote, like many other Tweets and memes, has a deep truth embedded in it, which made me realize that the majority of people bump into finance by necessity or on a one-off basis, instead of have it incorporated into their worldview. Whenever I started writing about the stock market to address the original question, I kept thinking: “Well before we can talk about that, we have to talk about this.” So let’s back up and do that.

Therefore, this post has two aims:

1) briefly explain how finance works in an intuitive and approachable way

2) broadly lay a financial & philosophical foundation to build off and serve as an easy self-contained reference for future discussions that may (realistically, will) involve markets, financial assets, and business

If you are a practitioner, feel free to either skip this one or use it as a refresher. If this is new to you, you can read it at any pace you choose. If you get it on your first try, you are ahead of the game.

The Main Concept

First, we start with some critical definitions. Finance is the management of money, which generally involves assets (things you own/control) and liabilities (things you owe). An asset is something of value that is expected to make money in the future. A few examples:

- coffee machine (a tangible asset; makes coffee that you can sell in the future)

- academic degree (an intangible or non-physical asset; signals you allegedly have the capability to do something an employer wants you to do, for which they would pay you)

- Netflix’s content licenses (they pay someone for the right to show their content (unless they make it themselves), then charge us monthly fees to see it – they are betting that over time you and I pay them more than it costs them to buy it)

- share of stock (an ownership interest in a business that entitles you to a share of the profits)

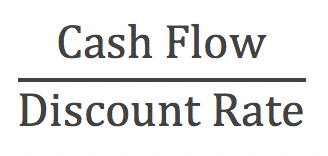

The value of every financial asset can ultimately be described by this formula:

Simple enough right? Well, the first kink in the hose is that the top number, cash flow, is uncertain because it takes place in the future. Cash flow is money coming in and out of an entity. If you make $10,000 a month in cash and spend $9,000 of cash, your cash flow is $1,000 per month. Same goes for a business.

Next, you may be asking “WTF is a discount rate?” I promised we would be quick, but the time value of money is so important in finance that we have to make sure we get it before we move on.

The good news is you already know it, you just might use different words or think about it less formally.

A Dollar Today is Worth More [To You] Than A Dollar Tomorrow

Aesop’s Sushi: A tuna in-hand is worth two in the ocean.

Suppose you have $100 and someone you know and trust (just enough) asks you for $100. You initially tell them to get lost because you’re going out for sushi tonight. But then, he/she/they sweetens the deal and says, “I’ll give you $110 tomorrow.” Now you’re interested because if you wait until tomorrow and he pays you back, not only can you get sushi, you can also get two coffees before brunch the following morning. The additional $10 is called interest and in this case it worked out to be 10% ($10 / $100). This is the part you know. But what about a reverse scenario, where you know you are going to get $110 tomorrow, but you want to figure out what that is worth to you today? This is called the present value. Essentially, you have to quantify the value of time (hard), the chance that you may not get the money (also hard), and what else you could do with that money (slightly easier and more fun, but still hard). That process is called discounting and the number is the rate at which you do it, hence discount rate. In this case, we may determine that the interest rate is the best discount rate, so we use the same 10% ($110 / 1.10 = $100).

When figuring out the present value, we put a 1 in the denominator plus the discount rate to get a smaller number. Without it, as in the first equation, we are assuming that the top number (cash flow) will go on forever and that the bottom number (discount rate) is the right number forever. That is called a perpetuity, but anyone offering you a perpetuity (money forever) is probably giving you a crummy deal, so we’ll skip that for now.

Therefore, the more realistic and complete present value formula is shown below. Before you get intimidated, take comfort knowing that you already solved it two paragraphs ago!

- m = number of payments per period (e.g. 1, 12, 365)

- n = number of periods over which the amount is being discounted

Cash flow: $110

Discount Rate: 10%

Number of payment periods (m): 1

Number of years (n): 1

Therefore, this simplifies to $110 / 1.10 = $100.

It is important to point out that there is nothing magical about the 10% number we used. If you get 10 cooks in a kitchen, you are going to get 10 recipes. The same is true in finance. If you ask 10 financiers at what rate they discount their cash flows, they too will give you 10 different answers.

We have mentioned in a previous post that in the publishing world, if you want to sell fewer books, include math in your writing. Unfortunately, if you want to make or keep money, you need to be numerate.

This chart takes the sushi example above, puts it into numbers, and extends it over a period of years instead of one day.

| Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| Cash Flow | $100 | $100 | $100 | $100 | $100 | $500 |

| Discount Rate | 10% | 10% | 10% | 10% | 10% | |

| Present Value | $90.91 | $82.64 | $75.13 | $68.30 | $62.09 | $379 |

In words, this table is saying we would feel exactly the same between taking $100 in one year or $90.91 today. If we increase (decrease) our discount rate, the amount we would be okay taking today gets smaller (bigger).

It is also implying that we would be okay taking $100 each year for the next 5 years or $379 today. Above, we mentioned the reasons we might make this trade-off: 5 years is a long time (sushi today is better than sushi tomorrow), what if the person we expect the $100 from can’t or won’t pay us (risk), and/or we may have something else we would rather do or somewhere else we could put the money that makes more than 10% per year (opportunity costs).

In the table above, we use the same discount rate, but obviously two years is twice as long, so you discount it twice, repeating the process as needed.

If this is the first time you have seen these calculations in your life, open the iPhone calculator app, turn the phone sideways so you get the expanded functions, and try doing this yourself. If you are really curious or want to know what your finance friends have been doing for most of their twenties, open up Excel and throw some of these in there.

Repetition for emphasis: This implies we would be indifferent between getting $379 today and $100 every year for 5 years. It is also implying we would pay $379 today to get $100 every year for 5 years.

Regardless of the complexity, whenever I’m scratching my head looking at something financial, I always try to figure out how it comes back to these main concepts above. Whether it’s $100 or $100,000,000, coffee sold or income earned, the formulas still apply.

The key distinction in the formulas we have talked about is whether you are going forward or backward in time – whether you want to see what money today is worth in the future or what money in the future is worth today.

- $100 x 1.10 = $110 (future)

- $110 / 1.10 = $100 (present)

I named this Part 1 because it is such an expansive subject we could end up like Idiosyncratic Whisk, whose most recent post is Housing: Part 306.

Whilst this is less exciting on the surface than endurance races, heists, or Kim Kardashian, finance is connected to (nearly) everything in the same way that Feynman’s divisions of scientific disciplines in the opening quote are connected. Finance is versatile – it allows you to do things like assess the validity of a politician’s claims (cough) and figure out if you’re getting screwed on your next loan to making sure you can afford sushi and wine.

Or, in keeping with Feynman’s instruction, it may be time to drink it and forget it all.

4 thoughts on “Finance: Part 1 (A Primer)”