Common interest rates & expected rates of return (Feb. 2020)

Prior Posts

Finance: Part 1 (A Primer)

Finance: Part 2 (Money, What Did You Expect?)

Interest Rate Basics

White people get money don’t spend it.

Or maybe they get money, buy a business.

I’d rather buy 80 gold chains and go ig’nant.

I know Spike Lee gon’ kill me but let me finish.

— Kanye West, Clique (2012)

Interest rates should be boring, until you understand them.

Many people find finance and economics concepts intimidating and, too often, unapproachable. Although this perspective is understandable, it is costly. The primary point of this series is to talk about finance in the real world, using simple terms.

You likely know most of this already. This post is intended to be a footnote in future finance discussions, avoiding the need to wander off to another website or grab a textbook.

Before we talk about the graphic, some reminders:

- Interest is money you pay for the right to borrow someone else’s money, or money you collect on money you lend out (known in the biz as “yield”).

Example: If you have a $30,000 loan on your car and it has a 3.00% interest rate, each year, you will pay the bank $900 in interest. - A rate of return is the total amount of money you make on your investments, expressed as a percentage of the investment’s initial cost.

Example: If your 401(k) (a self-directed retirement plan in the US) has $30,000 in it and one year later it is up to $33,000, your rate of return is 10% ($3,000 / $30,000).

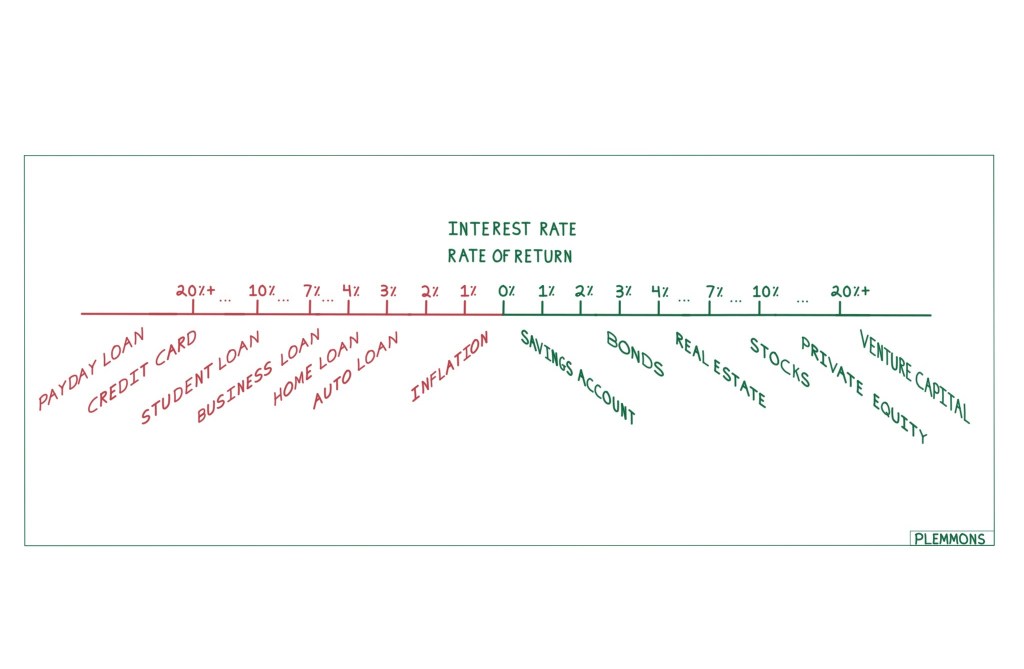

The Rates…or Spectrum of Trade-Offs

The graphic above shows common interest rates and expected rates of return for different loans and asset classes, at the time of this writing (these things change over time). I made it because people generally think about one thing at a time or the left side or the right side, but rarely zoom out to see the full continuum.

The connection between both sides is important. Obviously, there is someone else on the other side of every transaction, as this is the basis of commerce and double-entry accounting. Someone’s liability is someone else’s asset.

If someone pays you interest, that is your rate of return and vice versa.

Back to the graphic. It can be viewed as a simple comparison of rates and, maybe more importantly, as a spectrum of trade-offs.

What does that mean? In Part 1, we talked about how everything we do is a trade-off. By cooking at home instead of going out to eat, you are trading time (spent cooking) and fun for money (you saved by not going out).

Finance quantifies trade-offs. Money in a savings account is money that is not in real estate or stocks.

Starting at the center of the line (0%), as you move toward either side you see bigger numbers. Generally, the greater the return or interest rate, the greater the perceived risk. Risk means permanently losing your money. If something is not risk-free, then it means you can possibly lose your money (NOT FUN).

How Lenders Think

Using common sense, you would lend your most trustworthy friend more money than you would your least trustworthy friend. The least trustworthy one would have to offer you a higher rate or give you something valuable to hold onto (called collateral) in order for you to consider giving him your money instead of your more trustworthy friend.

Figuring out the risks is called underwriting or due diligence and tailoring the rate accordingly is called risk-based pricing. People who do these well get more return in relation to the risks they take.

There is a common misconception that if you are willing to take more risks, you will get a higher return. This makes no sense. If you reliably made more money taking more risk, then it wouldn’t be risky!

If you wanted to get a new tattoo and were short on ideas, you could use this one: NO ONE GIVES YOU RETURNS SIMPLY BECAUSE YOU ARE WILLING TO TAKE RISKS.

Imagine two runners about to start a marathon. One is hydrated and the other is dehydrated and left his shoes untied. The dehydrated one is taking more risk without any increase in reward.

If you want to understand how lenders must think, a quick math exercise will be helpful. If you make 100 $1,000 loans and you expect four of them (4%) to go bad (but, you don’t know which four), then you have to charge more than 4% to just get your money back.

| Step 1 | 100 loans x $1,000 each = $100,000 in total loans |

| Step 2 | $100,000 x 4.00% (interest rate) = $4,000 (interest you earned on all of the loans) |

| Step 3 | 4 loans do not get repaid x $1,000 = ($4,000) loss |

| Step 4 | Expected payoff: $4,000 (Step 2) – $4,000 (Step 3) = $0 |

To summarize:

- 96 of your 100 loans were repaid

- Only 4 were not repaid

- You made $0.

Normally, 96% accuracy is good! 96% accuracy shooting free throws will put you in the NBA Hall of Fame. That kind of accuracy in banking may lead to you looking for another job.

You either have to try charging more than 4% or collect more than 96% of the money you lent. We haven’t even gotten to competition. Imagine if your competitors were charging 4%, or less. In this scenario, with the same borrowers, you know that doesn’t make any sense, but if you refuse to make loans, how will you make any money?

Lending can be hard. You can see why people say the #1 Rule of Investing is: Don’t Lose Money.

The Examples, Briefly Explained

In finance, a good sign that things are working properly is when you cannot tell who is getting the better deal in a transaction (think sports betting).

I will give a short overview of each type of loan & investment to contextualize the rates associated with it. (Ownership in a company is called equity.)

- Savings account (0.0% — 2.50%): Money in a savings account at an FDIC-insured bank is risk-free up to $250,000. The bank pays you a guaranteed rate of return to give them your money. They take your money and lend it out.

- Inflation (0.0% — 2.50%): Increase in prices. If prices on everything you buy go up by 2% each year, you need to make 2% more just to buy the same things (maintaining your purchasing power). This is a hot button for your author and one we will revisit.

So here we are: This is a real trade-off you and I have to make every day. At best, our money in the bank is barely outpacing inflation. More likely, a year from now we will be able to buy less with it than we can right now. This is deeply frustrating because it feels like you always have to be doing something. We will get into the reasons for this another time.

Liabilities (If You Are the Lender, They Are Assets)

- Auto loan (3.00%+): Loans for vehicles. The narrative for the past couple decades is people need a way to get to work, so they’ll pay their car loans before anything else. Also, if you don’t pay your loan back, the bank can come take your car (the car is the bank’s collateral).

- Bonds (2.00% — 12.00%+): Debt from a corporation or government. If you lend money to Microsoft, there is a high probability they will pay you back. They know this, so they can borrow at 2%, roughly the same rate as the US Government. A distressed oil & gas company would have to offer a higher rate of interest to get us to lend to them. Some bonds have collateral (the business’s assets) and some are unsecured. You can think of those as a giant credit card.

Bonds are also referred to as fixed income. - Home Loan (3.5% — 6%+): Home mortgages. In this case, the house is the lender’s collateral. The government wants people to have houses, so rates are lower than they would be if the government was indifferent and not involved in the back-end of the process.

- Business Loan (2% — 12%+): There is one key difference between a bond and a loan. Bonds are generally designed to be traded among investors, like stocks. Most banks that make loans, keep them and earn the interest. There is almost always collateral.

- Student Loan (4 — 8%): Although there is no collateral, the government can garnish your wages if you don’t pay the loan back, which is arguably better (for them) than collateral.

- Credit Card (12% — 25%): An expensive tool for when you want to “buy 80 gold chains and go ig’nant.” No collateral. Capital One cannot take your gold chains if you ignore your credit card bill, but they will tell the credit reporting agencies, which will then reduce your credit score.

This has two negative consequences:

1) Lenders may be less willing to give you money

2) If they do, the interest rate on your new debt will be higher - Payday Loan (20%+): A short term loan, generally used for emergencies or drugs. These carry the highest interest rates because they are usually unsecured (no collateral) and are even riskier for the lenders than credit cards because fewer borrowers will be able to repay. If you are really interested in what this looks like in the US, check out Lisa Servon’s book, Unbanking of America.

Key takeaways

A lender expects a borrower to have a primary source of income (cash flow) to repay a loan. When they have a secondary source of repayment, collateral, it reduces their risk, because there are two ways of getting repaid instead of one, so they may be willing to offer a lower rate. If there is no collateral, the risk goes up, so you guessed it, the rate goes up.

- Primary source of repayment: Cash flow

- Secondary source of repayment: Collateral

Assets

The numbers in parentheses are expected rates of return. Remember, we said above that unless it is risk free, you can only guess in advance.

Expected return = Potential outcomes X the probability it happens

For example, if you bet $10 on a coin flip coming up heads, your expected return is $0 even though you will lose $10 or make $10.

Expected return = ($10 x 50% heads) + (-$10 x 50% tails) = $5 + (-$5) = $0

- Real Estate Investments (4.00%+): Equity in rental properties, apartments, office buildings, etc. You collect rent from your tenants and your total return = rental income – expenses + increase in the value of the real estate.

Real Estate Investment Trust (“REIT) is a hybrid between real estate investments and stocks. It is a company set up specifically to invest in a certain type of income-producing properties (real estate) and most of them are publicly traded, like a stock. You should expect to make less than you would if you owned the real estate directly because you have a professional management team doing the work for you, but you also likely can’t afford an entire New York City apartment building by yourself, so it gives you access to properties you otherwise would not have. - Stocks (5%+): Ownership/equity interests in public companies. Your rate of return is made up of dividends (the money the company pays out each year) + capital appreciation (how much the share price went up, or depreciation if it goes down!). Over a short period of time, stocks are riskier than bonds because the shareholders get the money leftover after the bondholders are paid.

- Private Equity (10%+): Ownership in a private business. The term usually has a specific context, compared to Private Businesses below. A team of financiers raises money from investors to buy a company with the goal of making it more valuable and selling it within 5-7 years. They usually take out substantial Business Loans to do this. When they sell the company and pay the loans off, the financiers and investors keep the rest of the proceeds.

- Venture Capital (20%+): Ownership interests in private businesses, usually with high growth potential. By now, you are skeptical. You know 20%+ returns have a catch. The catch: Many fail. The investors lose 100% of their money. Facebook was financed with venture capital. So was Juicero and Theranos. Minimal collateral.

- Private Businesses: Any business that isn’t publicly-traded. This includes everything from lawn mowing companies and restaurants to Cargill, the biggest private company in the US with $115 billion in revenue. I didn’t put any return expectations because it depends on so many things. Most business owners are trying to do some combination of making as much money as possible and trying to survive. Others, like Larry David in Season 10 of Curb Your Enthusiasm, opened up Latte Larry’s as a “spite store” only to put Mocha Joe out of business!

In Part 4, we will focus on risk.

See also:

- The Most Important Thing: Illuminated (Howard Marks)