— Michael Mauboussin, The Babe Ruth Effect

The frequency of correctness does not matter; it is the magnitude of correctness that matters.

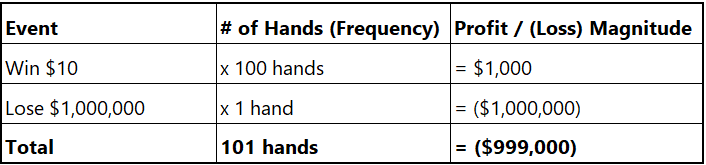

A simple example makes the point: You and I are playing Blackjack at the ARIA in Vegas. We bet $10 per hand and win 100 hands in a row. We may get interviewed by other players, the pit boss and some mathematicians…but not by Forbes.

Naturally, our confidence is through the roof, but we realize we have been betting like a couple of wimps. So, why aren’t we rich?

The only thing holding us back is our puny wager.

On the 101st hand, we up our bet to $1 million.

The dealer shows a face card.

We have 13. We hit…we get a King of Spades. We bust.

Despite a 99% success rate, we lost $999,000.

Our Profit & Loss

Clearly, our frequency of success is made irrelevant by the magnitude, or weighting, of the last hand.

We are wired to think a 99% success rate is good because it normally is. But, we just lost $999,000 with that same 99% success rate.

Most people struggle with this concept and even those who say they get it have a hard time incorporating it into their actions. Reversing the scenario shows why.

Opposite Scenario

Would you suffer losses 99% of the time for one big payoff?1

It is this instinctive aversion to losses that makes the appeal of the second scenario hard to accept.

We could use this simple hypothetical situation as a launching point for hours of conversation about asymmetry, options trading and uncertainty.

But, the part I want to focus on is using this idea to filter out noise in every part of your life.

Observing data, which is generally correct, logical, and scientific, can lead us to false conclusions if we don’t ask the relevant questions and see the complete picture.

The relevant question for Blackjack is: What was your total dollar profit?

We can quickly see how this could play out in real life.

Person 1: How did you do at the casino?

Person 2: I was on absolute FIRE. I won 100 hands of Blackjack in a row. Thinking about writing a book.

Person 1: So you won money?

Person 2: What do you mean, did I win? I just told you I won 100 hands in a row.

Person 1: Yeah, but what was your total dollar profit?

Everything is like this because every thought and activity has a weighting.

Most of the time, we weight things automatically. When we ask ourselves, “Is the extra storage in the iPhone worth another $200?” we are weighing the decision and coming up with an expected value in our head. When we say “It’s worth it,” we implicitly did an expected value calculation in our head.

When the weighting concept clicks, you will never look at anything the same.

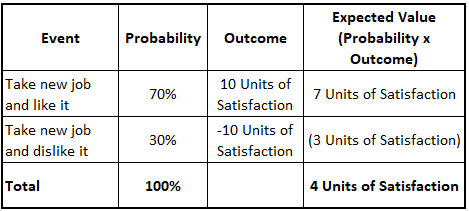

In another case, suppose you wanted to take a new job. The table below visually represents what we are thinking.

Expected Value (New Job)

Obviously, no one knows what a “unit of satisfaction” is exactly and what the actual probabilities are in advance. But, it is equally obvious that by laying it out, you can spot weaknesses in your assumptions, which will sharpen your thinking.

Trying to quantify complex emotions like satisfaction at a new job can be useful and shows the scope of the exercise, but it is hard and the outcomes resist precision.

So, let’s get back to where the outcomes are prominently countable: money.

Belief (Position) Sizing

Don’t tell me what you “think.” Tell me what you have in your portfolio.

Nassim Taleb, Skin in the Game

The closest thing we have to a window into someone’s soul is their investment portfolio (i.e. their actions). Even if you humbly acknowledge the future is unknowable, your financial portfolio forces a view because inaction is a choice. Sitting in cash? That tells me something. Fully invested in stocks? That tells me something. You only invest in real estate? You get the idea.

An opinion with nothing at risk is worthless. A valid question in finance is: How much money do you have on that idea?

The size (weight) of each position in your portfolio shows me your level of conviction in your idea.

The Robinhood trader telling you he made $4,000 on Tesla during quarantine wants you to focus on that one fact. He doesn’t want you to ask too many questions because he doesn’t want to tell you that he put most of his money into airline stocks and they’re down 50%.

(Note: If you are reading this on a phone, you may need to zoom in.)

He isn’t lying…but he isn’t telling you the whole truth. Although he made money on Tesla, his total portfolio is down 44%.

We learned from Blackjack that the size of the bet is at least as important as our skill and we learned from taking a new job that we should do things with a positive expected value.

This all seems straightforward right?

A question I get asked a lot made me realize that it isn’t: What do you think the stock market is going to do?

This question has made me develop a tremendous amount of empathy for good money managers because this requires a nuanced, probabilistic answer, but people crave simplicity. If you are managing these people’s money, the burden of providing easily digestible information is heavy.

As we just talked about, I can say “I don’t know,” but what he is really asking is: “What does your portfolio say the stock market is going to do?”

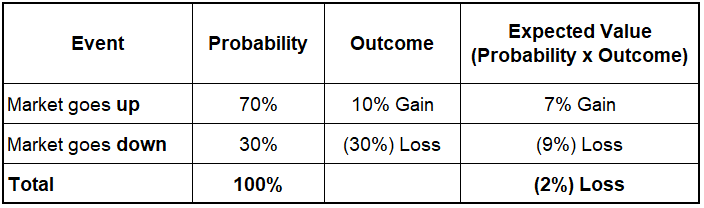

Thanks to Taleb and Howard Marks, I think about a range of possible outcomes, and I often draw a table, like the one below, on a whiteboard to show my thinking.2

Expected Value (Stock Market)

What should we do?

Here is a situation that is nearly as counter-intuitive as the opening Blackjack one: In this case, we should position ourselves for the market to go down, even though it is probably going to go up. The way to implement that idea is as critical as the insight, which may include over-weighting cash, buying put options, etc.

If you accepted this view as accurate, but stayed invested, a professional might say you are picking up pennies in front of a steamroller.

This is a more realistic version of the Blackjack dilemma. Everyone quickly sees why we lost money in Blackjack. This is a less salient experience because making money most of the time sure feels like we’ve made the right decision.

What if you were expecting to lose money most of the time, but over time your gains would offset your losses?

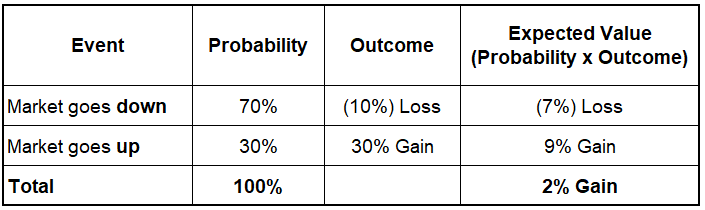

Opposite Scenario

Important note: This is not necessarily how I view the market. Of course, no one knows the ACTUAL probabilities of the outcomes (and there are an infinite number of outcomes). The point is to illustrate the how the weighting of the probability or outcome can change what you should do (the expected magnitude).

Position Sizing Continued

New scenario: You and I recouped our Blackjack losses and now we are eyeballing the stock market. After months of due diligence, we come up with five companies we want to invest in.

- Microsoft (MSFT)

- JP Morgan Chase (JPM)

- Berkshire Hathaway (BRKB)

- Walmart (WMT)

- LINN Energy (LINN)

At parties, we are indistinguishable because the only thing people have heard us talk about are these five companies, but no one has asked us the relevant questions from Blackjack: position sizing and total profits.

Let’s say Portfolio 1 is mine and Portfolio 2 is yours.

Investment Portfolio – Weighted Returns

Portfolio 1

Portfolio 2 (Same positions, different weights)

We both had the same analysis, same insights, and owned the same companies that were mostly winners, but because our position sizes (weights) were different, we had completely different experiences. You had an 81% return and I lost 6%.

In a world where outperforming by a couple of percentage points can attract billions of dollars, this is a material distinction.

As they say, God is in the detail. The weights are the details.

Of course all of our ideas are good and of course we’re right…but how right?

- Venture capitalists and equity investors talk about the Babe Ruth Effect because one investment with asymmetric returns can not only make up for a string of losses (“strikeouts”), it can make you permanently rich and famous.

- I thought this was a product of original thinking…I realized in writing this post that I got it from Nassim Taleb’s Fooled by Randomness, which I read in 2015. This happens often.

See also:

- The Babe Ruth Effect (Michael Mauboussin)

- Skin in the Game (Nassim Taleb)

- Superforecasting (Philip Tetlock)